2025 Annual General Meeting

Tuesday 11 November 2025

NAOS Ex-50 Opportunities Company Limited advises that its Annual General Meeting (AGM) will be held at 9.00 am (AEDT) on Tuesday 11 November 2025 at Castlereagh Room 1, Sheraton Grand Sydney Hyde Park, 161 Elizabeth Street, Sydney NSW 2000.

Further details relating to the AGM will be advised in the Notice of Meeting to be sent to all shareholders and released to the ASX immediately after dispatch.

In accordance with the ASX Listing Rules, valid nominations for the position of Director are required to be lodged at the registered office of the Company no later than 5.00 pm (AEST) on 16 September 2025.

FY25 Final Quarterly Dividend Dates

Ex-Dividend Date

Wednesday 10 September 2025

Record Date

Thursday 11 September 2025

Last Date for DRP Election

Friday 12 September 2025

Payment Date

Tuesday 30 September 2025

NAOS Investor Roadshow

The NAOS Investor Roadshow will be coming to a city near you this October. Join us as the investment team discusses its investment philosophy and process, and provides an outlook on the market. We will also highlight a selection of stocks that are held within our Listed Investment Companies (LICs).

We invite you to come along with a guest, meet us in person, and understand more about NAOS Asset Management (NAOS) and our LICs. Register today to secure your seat.

Adelaide

Thursday, October 9, 2025

10:30am - 12pm ACDT

The Playford Adelaide - MGallery

120 North Terrace

Adelaide, SA 5000

Perth

Thursday, October 16, 2025

10:30am - 12pm AWST

InterContinental Perth

City Centre, an IHG Hotel

815 Hay Street

Perth, WA 6000

Brisbane

Tuesday, October 21, 2025

10:30am - 12pm AEST

Sofitel Brisbane Central

249 Turbot Street,

Brisbane, QLD 4000

Melbourne

Tuesday, October 28, 2025

10:30am - 12pm AEDT

Hilton Melbourne

Little Queen Street

18 Little Queen Street

Melbourne, VIC 3000

Sydney

Thursday, October 30, 2025

10:30am - 12pm AEDT

Australian Museum

1 William Street

Darlinghurst, NSW 2010

Pre-Tax Net Tangible Assets per Share

Post-Tax Net Tangible Assets per Share

FY25 Dividend (cents per share)

Dividend Yield

Share Price

Shares on Issue

Convertible Note Price (ASX: NACGA)

Convertible Notes on Issue

Directors’ Shareholding (number of shares)

Profits Reserve (cents per share)

NAC Investment Portfolio Performance* | S&P/ASX 300 Industrials Accumulation Index | Performance Relative to Benchmark | |

|---|---|---|---|

1 Year | +28.92% | +18.90% | +10.02% |

3 Years (p.a.) | +3.13% | +16.04% | -12.91% |

5 Years (p.a.) | +5.13% | +12.58% | -7.45% |

10 Years (p.a.) | +7.82% | +8.73% | -0.91% |

Inception (p.a.) | +8.23% | +8.72% | -0.49% |

Inception (Total Return) | +131.81% | +143.26% | -11.45% |

Sarah Williams was appointed as an Independent Director in January 2019 and was elected Independent Chair on 1 December 2022. Sarah is also the Independent Chair of NAOS Emerging Opportunities Company Limited (ASX: NCC) and an Independent Director of NAOS Small Cap Opportunities Company Limited (ASX: NSC).

Sarah has over 25 years’ experience in executive management, leadership, IT and risk management in the financial services and IT industries. Most recently, Sarah was an executive director at Macquarie Group and head of IT for the group’s asset management, investment banking and leasing businesses. During her 18-year tenure at Macquarie Group, she also led the Risk and Regulatory Change team and the Equities IT team and developed the IT M&A capability. Sarah has also held senior roles with JP Morgan and PricewaterhouseCoopers in London.

Sarah has also been a director of charitable organisations including Cure Cancer Australia Foundation and Make a Mark Australia. Sarah holds a Honours Degree in Engineering Physics from Loughborough University.

Sebastian Evans has been a Director of the Company since its inception. Sebastian is also a Director of NAOS Emerging Opportunities Company Limited (ASX: NCC), NAOS Small Cap Opportunities Company Limited (ASX: NSC), and has held the positions of Chief Investment Officer (CIO) and Managing Director of NAOS Asset Management Limited, the Investment Manager, since 2010.

Sebastian is the CIO across all investment strategies. He holds a Master of Applied Finance (MAppFin) majoring in investment management, as well as a Bachelor of Commerce majoring in finance and international business, a Graduate Diploma in Management from the Australian Graduate School of Management (AGSM) and a Diploma in Financial Services.

David Rickards OAM has been an Independent Director of the Company since its inception. David is also the Independent Chair of NAOS Small Cap Opportunities Company Limited (ASX: NSC). He is also Co-Founder of Social Enterprise Finance Australia Limited (Sefa) and was a director and treasurer of Bush Heritage Australia for nine years.

David has over 25 years of equity market experience, most recently as an executive director at Macquarie Group, where he was head of equities research globally, as well as equity strategy from 1989 until he retired in mid-2013. David was also a consultant for the financial analysis firm Barra International.

David holds a Master of Business Administration majoring in accounting and finance from the University of Queensland. He also has a Bachelor of Engineering (Civil Engineering) and a Bachelor of Engineering (Structural Engineering) from the University of Sydney, and a Bachelor of Science (Pure Mathematics and Geology).

Warwick Evans has been a Director of the Company since its inception. Warwick is also a Director of NAOS Emerging Opportunities Company Limited

(ASX: NCC), NAOS Small Cap Opportunities Company Limited (ASX: NSC) and Chair of NAOS Asset Management Limited, the Investment Manager.

Warwick has over 35 years of equity market experience, most notably as Managing Director of Macquarie Equities (globally) from 1991 to 2001, and as an executive director for Macquarie Group. He was founding Chairman and CEO of the Newcastle Stock Exchange (NSX) and was also Chairman of the Australian Stockbrokers Association. Prior to these positions, Warwick was an executive director at County NatWest.

Warwick holds a Bachelor of Commerce majoring in economics from the University of New South Wales.

Dear fellow shareholders,

On behalf of the Board, welcome to the Annual Report of NAOS Ex-50 Opportunities Company Limited (Company) for the financial year ended 30 June 2025. We extend our appreciation to all shareholders for your continued support and warmly welcome new shareholders who joined us in FY25.

The past 12 months have been defined by a shifting economic environment, with the RBA cutting interest rates in late 2024 and early 2025 to bolster economic activity, offset by volatile commodity prices, lagging inflationary pressures and a volatile macro backdrop. What did remain constant was the continued demand for large and liquid listed businesses, which saw the continued outperformance of the largest listed businesses in Australia.

Despite this backdrop, NAC delivered a +28.92% investment return for FY25, significantly outperforming the S&P/ASX 300 Industrials Accumulation Index return of +18.90%.

The Company reported a $7.55 million after-tax profit, a marked turnaround from the $13.31 million loss in FY24. The Board has declared a final quarterly dividend of 1.50 cents per share (50% franked), bringing the total FY25 dividend to 6.0 cents per share, comprising two fully franked and two 50% franked dividends.

This dividend marks the 11th consecutive year NAC has maintained or increased its annual dividend and represents a 12.77% yield, based on the 30 June 2025 closing share price of $0.47. Since inception, NAC has declared 57.15 cents per share in dividends, or 80.43 cents on a grossed-up basis, with the majority fully franked.

NAC’s strong profits reserve of 47.95 cents per share provides a strong foundation to deliver sustainable, tax-effective income to shareholders in future periods.

NAC Dividend History

In FY25, the pre-tax Net Tangible Asset backing (NTA) per share of the Company increased from $0.54 to $0.67 over the financial year, as shown in the following chart.

NAC Pre-Tax NTA Performance

Throughout the year, the Board maintained its implementation of a disciplined capital management strategy focused on maximising long-term shareholder value:

Each of these measures is part of a clear, disciplined capital allocation framework designed to support sustainable shareholder outcomes.

Importantly, alignment between shareholders, Directors, and the Investment Manager continues to strengthen. Directors and staff of the Investment Manager now hold 9.3 million NAC shares, and the Manager’s Fee Reinvestment Commitment, introduced in FY24, remains in place.

Despite broader market preferences leaning towards large-cap exposures, NAC’s differentiated strategy focusing on underappreciated businesses outside the ASX 50 positions us to continue delivering attractive long-term outcomes for shareholders.

On behalf of the Board, thank you once again for your ongoing trust and support.

Kind regards,

Sarah Williams

Independent Chair

21 August 2025

Dear fellow shareholders,

For the financial year ending 30 June 2025 (FY25), the NAC Investment Portfolio increased by +28.92% compared to the Benchmark S&P/ASX 300 Industrials Accumulation Index (XKIAI), which increased by +18.90%. After a tumultuous FY24, it was pleasing to produce a strong positive return, which more than offset the losses generated in FY24. It is equally rewarding to have achieved the majority of this performance from our core investments, which we steadfastly held throughout FY23 to FY25.

The NAOS team firmly believed that the core fundamentals of our investments would continue to strengthen over time, and we were confident that share prices would eventually reflect this strength, despite some delay. As noted below and in my closing outlook, despite significant share price appreciation, the valuations of most, if not all, of our core investments remain below their full potential. In fact, we believe these investments are derisking, thereby enhancing their long-term valuation potential.

Relevance, Momentum and Index Inclusion

Reflecting on my FY24 Investment Manager’s Report, I dedicated significant discussion to the distinctive market dynamics that emerged, where valuations were often overshadowed by the influence of passive capital flows and index inclusion. A prime example was the share price of Commonwealth Bank of Australia Ltd (ASX: CBA), which soared to a record valuation despite maintaining a flat earnings per share (EPS) profile for several years.

Fast forward to the end of FY25, and this market dynamic, if anything, has only strengthened, and generally equity investors of all types are being forced to ‘play the game’ and therefore focus on companies that form part of the index or are a good chance of index inclusion in the short term.

Turning to CBA, its share price, excluding dividends, has increased by +46% in FY25, following a 37% increase in FY24, marking the seventh consecutive year of share price growth. For further context, the chart below compares the grossed-up yield of CBA shares to Australian Government 10-year bond yields over a 10-year period. As the chart illustrates, despite CBA’s flat profit growth outlook, its shares are arguably being priced similarly to a government bond. This suggests investors perceive CBA’s risk profile as being closely correlated with the Australian government’s balance sheet.

Commonwealth Bank vs Australian 10 Year Bond - Yield

CBA has several qualitative attributes that continue to drive its rising valuation. In our view, these include:

From a NAOS standpoint, we will continue to focus on what we can control. Our investment philosophy centres on investing in emerging companies that deliver high returns on invested capital and are led by experienced, aligned management teams. These companies operate in industries poised for sustained revenue growth, where they hold clear competitive advantages, and their business models are transparent to investors. Notably, 100% of NAC’s portfolio is outside the ASX indices, ensuring our investments diverge significantly from the benchmark, the S&P/ASX 300 Industrials Accumulation Index.

Below, I have expanded upon several core investments within the NAC investment portfolio, outlining why we believe these companies have the potential to generate significant long-term value for shareholders irrespective of their share price movements in FY25.

Urbanise.com (ASX: UBN) – Strategic Partnership with National Australia Bank (ASX: NAB)

UBN has been an investment within the NAC Investment Portfolio for over four years. Our investment thesis centres on the strength of UBN’s strata management software, which it successfully developed and brought to market.

Prior to our involvement, UBN underwent several iterations, and, like many ASX-listed companies, suffered from misguided strategic decisions by former board members and management. These missteps, in our view, led to a loss of focus and significant capital waste, resulting in accumulated losses exceeding $100 million on the balance sheet.

Since our involvement as investors, UBN has shown notable progress. A pivotal catalyst for this turnaround was the appointment of Darc Rasmussen as Director and subsequently Chairman, coupled with the replacement of most prior Directors and the addition of another Independent Director. We believe these changes were critical in sharpening UBN’s strategic focus, reinforcing its commitment to its strata management software, and addressing both industry needs and deficiencies in its own platform.

This strategic shift culminated in May 2025, with the signing of a strategic partnership with Australia’s largest business bank, National Australia Bank Ltd (ASX: NAB). Key highlights of this partnership include:

UBN and NAB will seek to deliver a best-in-class service for strata managers and their clients by integrating UBN’s fully cloud-based strata management software with NAB’s tailored banking solutions designed to address the specific needs of the strata industry. For context, there are approximately 2.3 million strata-titled properties (also known as lots) in Australia, underscoring the significant market potential for this offering.

Body corporates, also known as the Owners Corporations, are a mandatory component of a strata scheme, which comprises multiple strata-titled properties. These entities must maintain bank accounts to collect strata levies from lot owners and facilitate payments for various expenses, including cleaning, maintenance, and capital works programs. Typically, these accounts are divided into an Admin Fund and a Capital Works (or Sinking) Fund. A strata manager, appointed by the body corporate, oversees the management and accounting of these accounts.

Based on publicly available information, we estimate the average funds held in body corporate bank accounts are approximately $3,500 per lot. Applied to Australia’s ~2.3 million strata-titled properties, this suggests around $8 billion in deposits within strata-related accounts. We believe this estimated quantum of funds within strata bank accounts may even be conservative.

Public data suggests that over 70% of the strata-related bank deposit market is held by one major Australian bank, which also processes a significant portion of the associated payments. We also believe there is a high level of fees associated with said payments.

Banks use customer deposits to fund a portion of the loans they provide (e.g., mortgages, car loans), generating a net interest margin (NIM) by lending at higher rates than those paid on deposits. Strata-related bank accounts, which typically earn low deposit rates, allow banks to achieve a higher-than-average NIM on these funds. Consequently, a bank with a significant share of the strata deposit market benefits from a substantial cost advantage and a stable, low-cost funding base, particularly when compared to term deposits, which may cost banks approximately 4-5% annually.

The 2024 Macquarie Strata Management Benchmarking Report indicates that only ~22% of Australian strata managers qualify as ‘higher-performing businesses’. According to the report, a key aspect of a higher-performing business is its investment in technology to create operational efficiencies and generate materially higher profit margins than the industry average.

It is no surprise that the strata industry is generally characterised by legacy technology systems, both from a strata banking perspective and a strata management perspective. We estimate that ~60% of strata managers rely on outdated DOS/Windows or on-premises software systems, which limit scalability and efficiency, forcing firms to hire more staff to manage growth. Consequently, as shown in the chart below, average profit margins in strata management have declined steadily over the past two decades.

Strata Managers - Average Profit Margin

The opportunity for UBN’s strata division lies in addressing these challenges, with revenue potential driven by three key factors:

1. Software Revenue Growth – At the close of FY25, UBN generated over $7 million in recurring revenue, purely from its strata management software, holding an estimated ~15% market share in Australia with a historical growth rate of ~3% per annum. Should the NAB payments portal gain traction within the strata management industry, we anticipate accelerated growth as managers adopt UBN’s software alongside NAB’s potentially best-in-class payment platform to maximise efficiencies. The chart below shows the potential based on the total lots in Australia.

Number of Strata Lots Using Software

2. Recurring Revenue from the NAB Payments Platform – Starting in FY26, UBN will receive a fixed recurring fee of $1.3 million from NAB for maintaining the payments platform. Additionally, UBN may receive variable recurring fees tied to the volume of strata-related bank accounts held with NAB. With an estimated $8 billion in strata deposits, UBN’s recurring revenue is expected to be tied to a portion of the net interest margin (NIM) generated from these deposits. UBN has publicly projected this opportunity at approximately $50 million annually, equivalent to an interest cost of ~0.625%.

3. Market Consolidation – Over the longer term, consolidation among strata software providers presents a compelling opportunity. With 3-4 providers each holding 15-20% market share, UBN stands out as the only major player with a fully cloud-based platform. Providers with legacy systems face a critical choice: invest heavily in cloud migration or merge with a provider like UBN that already offers a scalable, modern solution.

Looking forward, we believe UBN has the potential to generate more than $20 million p.a. in recurring revenue from its strata-related products over the next 3-5 years, with incremental revenue expected to deliver progressively higher margins. Importantly, this recurring revenue in theory will be very sticky, potentially commanding a premium valuation multiple in the market.

The next 12-18 months will be critical in determining the success of the UBN-NAB partnership and whether the strata industry truly understands the real benefits to them and their clients.

COG Financial Services (ASX: COG) – Board Overhaul and Strategic Reset

In last year’s letter, I outlined the critical changes we felt were necessary for COG to restore shareholder value and establish a sustainable path to growing earnings per share (EPS). Through early FY25, COG persisted with its prior strategy, resulting in a share price decline from $1.10 to a low of $0.86 in March 2025.

COG Financial - Share Price & Key Events

This trajectory shifted dramatically following a significant board overhaul: three directors, including the Chair, resigned, one transitioned to a non-executive role, and two new non-executive directors were appointed, with one assuming the Chair position. To support this transition, NAOS and other major shareholders sold a significant portion of their holdings, which enhanced liquidity in COG shares and enabled new directors and institutional investors to acquire meaningful stakes. We believe owning a smaller share of a revitalised, high-potential business is preferable to a larger stake in an underperforming company with limited prospects for improvement.

The most notable outcome of all the changes mentioned above was the appointment of Tony Robertson as Chair and John Dwyer as a Non-Executive Director. These appointments are significant for several reasons:

PSC Insurance - Share Price

With the new Board in place, COG has swiftly advanced its simplification strategy. The sale of minority stakes in Earlypay Ltd (ASX: EPY) and Centrepoint Alliance Ltd (ASX: CAF) has generated ~$25 million in cash proceeds. The remaining step in this simplification effort, in our view, is addressing the Westlawn Group, COG’s asset management business. We believe this business contributes less than $2 million to group profitability but adds significant complexity to the balance sheet and cash flow statement due to Westlawn’s debenture program. If this business were to be sold, it would enable current and prospective shareholders to clearly see the capital-light nature and strong free cash flow generated by COG’s core operations.

Ultimately, for COG to achieve long-term success, it must deliver consistent organic earnings growth, even if that growth rate is ~5-10% p.a. While the full strategy is yet to be disclosed, we anticipate that Robertson and Dwyer’s insurance broking expertise will drive improvements in COG’s underdeveloped insurance broking division. Given the thousands of finance broking transactions that occur through a COG-owned or aligned broker, the potential for cross-selling insurance products is substantial.

At the very least, we believe COG now has a credible opportunity to unlock its full potential as Australia’s largest finance, broking & aggregation business. While its ultimate scale and valuation remain uncertain, comparable businesses with steady organic growth and strategic acquisitions have historically commanded premium earnings multiples. Accordingly, COG’s future valuation could be significant, provided it executes effectively under its revitalised leadership.

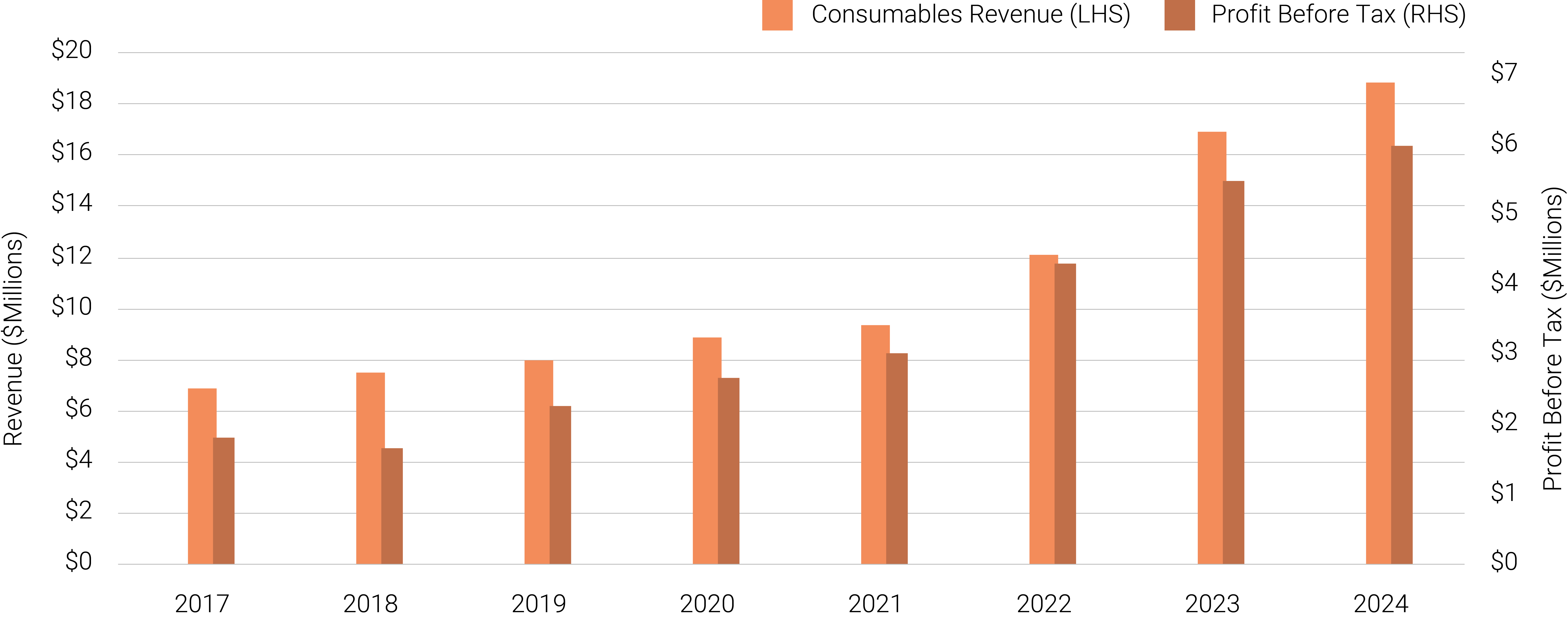

XRF Scientific (ASX: XRF) – New Core Investment

XRF Scientific stands out as an emerging company that has sustained consistent growth over the past five to ten years without significant equity issuance. Over the last decade, XRF has achieved compound annual revenue growth of ~10.6% and EPS growth of ~12.9%.

XRF Scientific - EPS & Return on Invested Capital (ROIC)

Founded in 1972 and listed on the ASX in 2007, XRF manufactures equipment and chemicals for sample preparation and analysis, serving production mines, construction companies and commercial analytical laboratories around Australia and globally. Its revenue model comprises upfront equipment sales and recurring consumable sales, the latter critical for maintaining machine performance in high-stress environments (e.g., extreme heat). In our view, XRF’s competitive edge lies in its unique ability to supply both equipment and consumables across the entire sample preparation workflow, unlike peers who typically offer only partial solutions.

In FY25, XRF is projected to deliver ~$60 million in revenue and ~$9.4 million in NPATA, with operating margins expanding from 5-8% five years ago to over 23% today. We attribute this margin growth to a new manufacturing facility in Melbourne, operational since circa 2019, as well as the increasing proportion of high-margin consumable sales, driven by the growing number of XRF machines in the market.

XRF Consumables Revenue & Profit Before Tax

Given XRF’s premium valuation, driven by its high-quality attributes, our focus is on how XRF can sustain revenue growth greater than 8% annually for the foreseeable future. We believe the following strategies will drive this growth:

Outlook for FY26

At our October 2024 national roadshows, we emphasised the goal of delivering a +10-20% return for the NAC portfolio in FY25, supported by the low valuations of our core holdings and modest earnings growth projections.

We are pleased to deliver a return of ~30% in FY25. This is further underscored by the promising outlook for our core holdings, particularly given their current valuations.

Below, I outline the key value-creating catalysts for select portfolio companies, underscoring their medium-term potential despite significant FY25 share price gains:

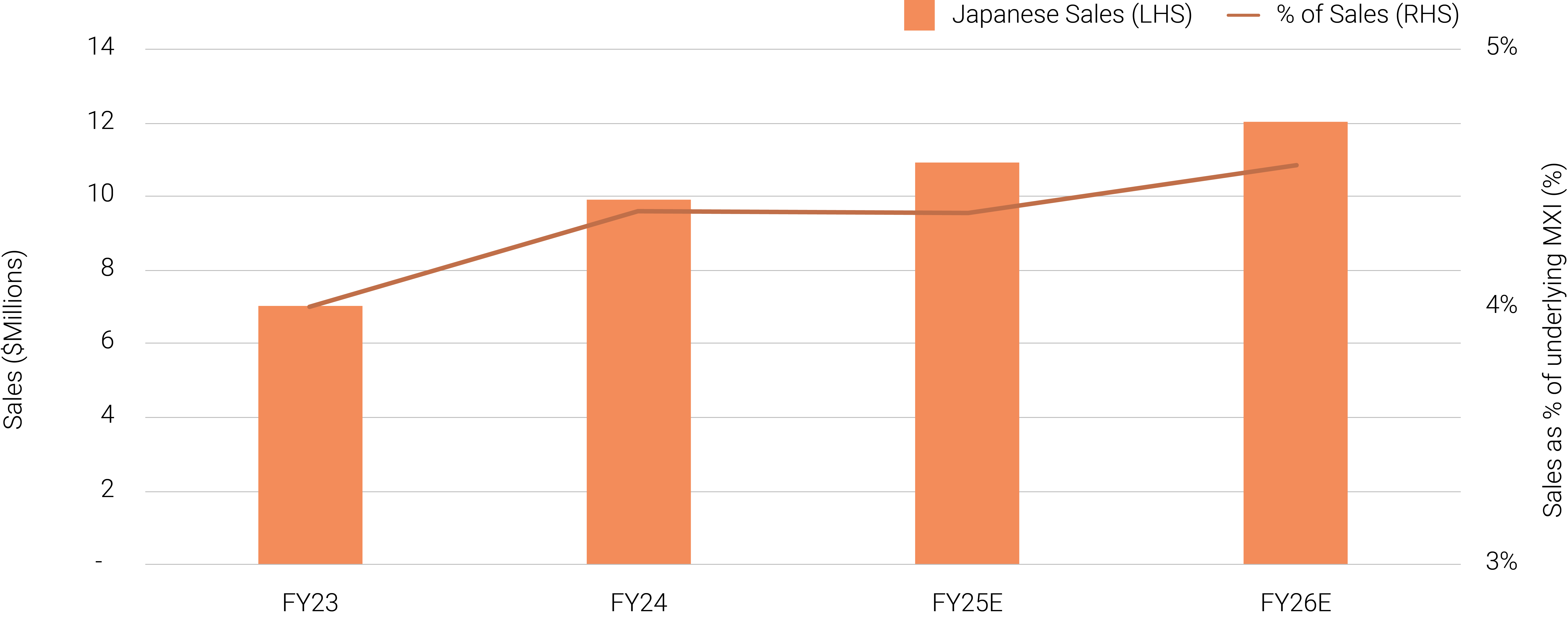

MaxiPARTS (ASX: MXI)

MXI’s Japanese Sales

Bravura Solutions (ASX: BVS)

Urbanise.com (ASX: UBN)

COG Financial Services (ASX: COG)

MOVE Logistics (NZX/ASX: MOV)

While the catalysts outlined above may seem granular, we believe their realisation in FY26 could drive significant shareholder value, particularly if accompanied by a valuation re-rating and sustained earnings growth. This underpins our conviction that the intrinsic value of our investments far exceeds their current share prices, even after NAC’s impressive +28.92% portfolio return in FY25.

I look forward to updating you over the next 12 months on the progress of these investee companies concerning these catalysts, and we remain confident that many should materialise as anticipated. The NAOS team and I remain steadfastly committed to delivering sustainable, positive returns for all NAC shareholders through a concentrated portfolio of Australian and New Zealand emerging companies.

I would also like to acknowledge our long-standing NAC shareholders for their unwavering support, particularly during periods of performance volatility. As a sign of my confidence in NAC’s long-term value creation, I have continued to acquire shares and will do so as long as this potential remains.

Kind regards,

Sebastian Evans

Managing Director and Chief Investment Officer

NAOS Asset Management Limited

MOVE Logistics (MOV) is one of the largest freight and logistics providers in New Zealand, with its origins dating back to 1869. With a team of more than 1,100 experts, the business provides end-to-end supply chain services and has the capability to serve more than 3,500 customers across its large network, which includes 40 branches spread across the two main islands of New Zealand.

movelogistics.com

MaxiPARTS (MXI) is a supplier of commercial truck and trailer aftermarket parts to the road transportation industry. In operation for over 30 years, MXI is one of the largest operators in Australia, with a unified support and distribution network providing over 162,000 different parts across 29 sites nationwide.

maxiparts.com.au

XRF Scientific Limited (XRF), based in Perth, Australia, manufactures equipment and chemicals which is used in the preparation of samples for analytical testing and quality control. With facilities in Australia, Europe, and Canada, plus global distributors, their products are distributed globally and used by miners, construction companies and commercial analytical laboratories.

xrfscientific.com

Urbanise.com (UBN) is an Australia-headquartered cloud-based software business, providing solutions for both the strata management industry as well as the facilities management industry in the Asia–Pacific and Middle East regions. The Urbanise Strata Platform is a market-leading accounting and administration software system used by strata managers across ~650,000 individual strata lots. The Urbanise Facilities Management Platform is used to aid the maintenance of property assets and supervision of contractors across various sectors, including aged care, retail, commercial and essential infrastructure.

urbanise.com

COG Financial Services (COG) is Australia’s leading aggregator of finance brokers and equipment leasing services to small and medium-sized enterprises (SMEs). COG’s operations are spread across three complementary business divisions: Finance Broking & Aggregation (FB&A), Lending & Funds Management, and Novated Leasing, all of which service the financial needs of SMEs nationwide. As at the end of FY24, COG had a ~21% market share of the Australian Asset Finance Broking market, with the COG network financing $8.9bn in assets for SMEs in FY24. COG has been highly acquisitive in recent years, acquiring finance brokers, insurance brokers, as well as funds management and novated leasing businesses.

cogfs.com.auNAOS Asset Management is a specialist fund manager that provides concentrated exposure to quality Australian and New Zealand emerging companies.

NAOS takes a concentrated and long-term approach to investing and aims to work collaboratively with businesses rather than be a passive shareholder. NAOS seeks to invest in businesses with established moats and significant exposure to structural industry tailwinds, which are run by proven, aligned and transparent management teams who have a clear understanding of how to compound capital.

We aim to make significant investments in businesses and, on occasion, seek board representation or appoint highly regarded independent directors. Importantly, NAOS, its Directors and staff are significant shareholders in the NAOS LICs, ensuring strong alignment with all shareholders.

NAOS is B Corp Certified. As a B Corp in the financial services industry, we are counted among businesses that are leading a global movement for an inclusive, equitable and regenerative economy.

NAOS launched its first LIC in 2013 with 400 shareholders. Today, NAOS manages three LIC vehicles and one private investment fund for approximately 6,000 shareholders.

We believe in investing in businesses where the earnings today are not a fair reflection of what the same business will earn over the longer term. Ultimately, this earnings growth can be driven by many factors, including revenue growth, margin growth, cost cutting, acquisitions and even share buybacks. The result is earnings growth over a long-term investment horizon, even if the business was perceived to be a value-type business at the time of the initial investment.

Excessive diversification, or holding too many investments, may be detrimental to overall portfolio performance. We believe it is better to approach each investment decision with conviction. In our view, to balance risk and performance most favourably, the ideal number of quality companies in each portfolio would generally be zero to 20.

As investors who are willing to maintain perspective by taking a patient and disciplined approach, we believe we will be rewarded over the long term. If our investment thesis holds true, we persist. Many of our core investments have been held for three or more years, where management execution has been consistent and the value proposition is still apparent.

We believe in backing people who are proven and aligned with their shareholders. One of the most fundamental factors consistent across the majority of company success stories in our investment universe is a high-quality, proven management team with “skin in the game”. NAOS Directors and employees are significant holders of shares on issue across our strategies, so the interests of our shareholders are well aligned with our own.

This means we are not forced holders of stocks with large index weightings that we are not convinced are attractive investment propositions. We actively manage each investment to ensure the best outcome for our shareholders, and only invest in companies we believe will provide excellent, sustainable, long-term returns.

As a specialist fund manager since 2004, over the years NAOS has developed a strong “circle of competence” (or mental models) in specific industries. We openly acknowledge we avoid businesses that are either too complex to understand, or heavily influenced by one or two variables, such as interest rates or commodity prices. Instead, we concentrate on businesses that fall within our circle of competence, aiming to minimise the risk of permanent capital loss. Unlike others, we are comfortable setting aside investments that we consider “too hard”, while we compound our knowledge in specific industries where we believe we have a competitive edge.

We believe in taking advantage of inefficient markets. The perceived risk associated with low liquidity (or difficulty buying or selling large positions) combined with investor short-termism, presents an opportunity to act based purely on the long-term value proposition, where the majority may lose patience and move on. Illiquidity is often caused by aligned founders or management having significant holdings in a company. The NAOS LICs benefit from a closed-end structure, which means they do not suffer “redemption risk” and we can focus on finding quality, undervalued businesses regardless of their liquidity profile.

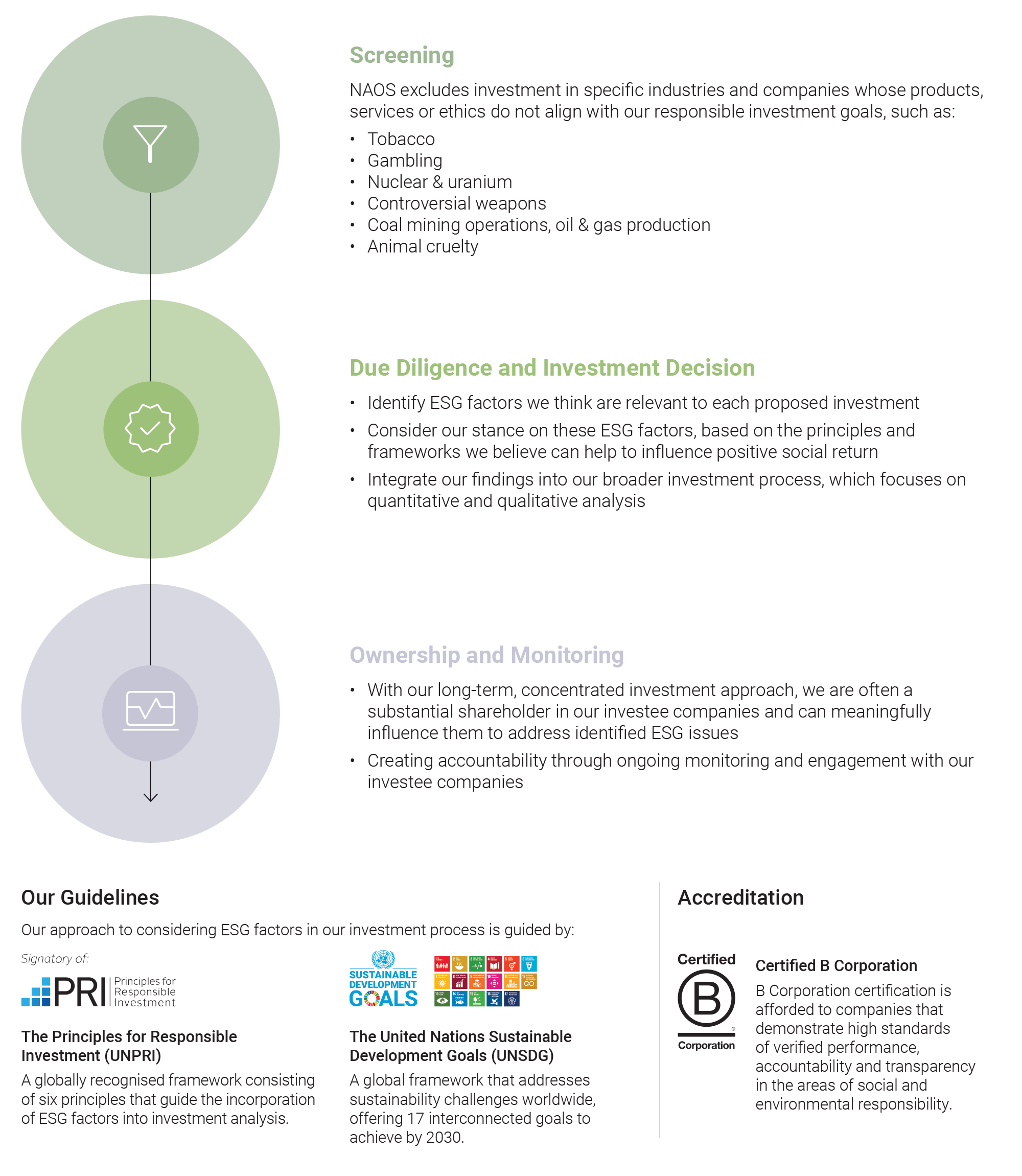

As an investment manager, NAOS recognises and accepts its duty to act responsibly and in the best interests of shareholders. We believe a high standard of business conduct and a responsible approach to environmental, social, and governance (ESG) factors is associated with a sustainable business model over the longer term. This benefits not only shareholders, but also the broader economy. NAOS is a signatory to the United Nations-supported Principles for Responsible Investment (UNPRI) and is guided by these principles in incorporating ESG into its investment practices. NAOS is also B Corp certified.

At NAOS, we seek to work collaboratively with businesses and their respective management teams. We are often the largest shareholder in the businesses we invest in, and from time to time we will seek board representation, either via an independent or a non-independent representative. This approach allows us to supportively engage with the boards and/or management teams of our portfolio holdings, and maximise the potential for our invested capital to compound at a satisfactory rate over the long term.

Examples of constructive engagement where the NAOS investment team looks to add value include:

Company Size & Security Type

Remove: ASX Top 50, <$20m market cap, ETFs

Revenue

Remove: No substantial revenue

Industry

Remove: Industries in structural long-term decline and not conducive to long-term growth

ESG Negative Screen: Tobacco, Gambling, Nuclear and Uranium, Controversial Weapons, Coal Mining Operations, Oil and Gas Production and Animal Cruelty

Balance Sheet

Remove: Unsustainable debt levels

Management & Culture

Valuation, Growth & Margin of Safety

Considering ESG Factors

ASX: NCC NAOS Emerging Opportunities Company Limited

NCC generally invests in 0-20 Australian and New Zealand emerging companies.

ASX: NAC NAOS Ex-50 Opportunities Company Limited

NAC generally invests in 0-20 Australian and New Zealand emerging companies.

ASX: NSC NAOS Small Cap Opportunities Company Limited

NSC generally invests in 0-20 Australian and New Zealand emerging companies.

NAOS also follows this Investment Criteria when investing in private emerging companies.

The NAOS investment team undertakes fundamental analysis on potential and current investments. Some examples of key focus areas include:

At NAOS, as an investment manager, we recognise and accept our duty to act responsibly and in the best interests of all stakeholders. We believe that a high standard of business conduct and a responsible approach to environmental, social and governance (ESG) factors are associated with a sustainable business model over the longer term, which also benefits the broader economy.

We recognise the material impacts that ESG factors can have on investment returns and risk, and also the wider implications for achieving a positive social return.

At NAOS Asset Management, we believe in providing shareholders with meaningful insights into the companies in which we invest. We recently spoke with Peter Loimaranta, Chief Executive Officer of MaxiPARTS Limited. The discussion covered industry trends, operational strengths, and how MaxiPARTS is positioned for sustainable growth.

How does Australia’s ageing vehicle fleet affect demand?

Australia has one of the oldest commercial fleets in the developed world, with heavy vehicles now averaging 16 years. As trucks age, more maintenance is done outside dealer networks, driving demand from MaxiPARTS’ core customers: independent repairers and operators. Structural trends, such as rising confidence in aftermarket products and the growing share of aftermarket spend, continue to support long-term growth.

How does MaxiPARTS build lasting customer relationships?

We focus on delivering value through the right people, strong stocking strategies, and competitive pricing. Our services—like just-in-time scheduling, embedded staff, inventory systems (MaxiSTOCK), and consignment stock—are tailored to meet the specific needs of fleet operators, workshops, and manufacturers.

What are the most significant operational challenges?

With thousands of vehicle types and parts, cataloguing and accessibility are major challenges. We work closely with suppliers to access product data and training, and we’re now exploring the use of AI to enhance parts identification and internal systems.

What role do electrification and autonomy play in your outlook?

These trends are emerging but remain medium- to long-term. Our broad product range helps protect against near-term shifts while positioning us to adapt as demand for new technologies grows. We’re already working with suppliers to understand evolving replacement needs.

How does MaxiPARTS’ strategy support above-average, risk-adjusted returns over the medium to long term?

Through a combination of strategic acquisitions (e.g. Truckzone, Förch, Independant Parts) and organic growth, we’ve expanded our product range, increased scale, and diversified revenue. We focus on higher-margin growth areas like our Japanese parts and Förch businesses while maintaining strong cash flow, low gearing, and consistent dividend distribution. This disciplined approach supports sustainable, risk-adjusted returns.

Sebastian is a Director of NAOS Emerging Opportunities Company Limited (ASX: NCC), NAOS Small Cap Opportunities Company Limited (ASX: NSC), NAOS Ex-50 Opportunities Company Limited (ASX: NAC), and has held the positions of Chief Investment Officer (CIO) and Managing Director of NAOS Asset Management Limited, the Investment Manager, since 2010. Sebastian is the CIO across all investment strategies.

Sebastian holds a Master of Applied Finance (MAppFin) majoring in investment management, as well as a Bachelor of Commerce majoring in finance and international business, a Graduate Diploma in Management from the Australian Graduate School of Management (AGSM) and a Diploma in Financial Services.

Robert joined NAOS in September 2009 as an investment analyst. Robert has been a portfolio manager since November 2014 and is currently Portfolio Manager across all NAOS LICs: NAOS Emerging Opportunities Company Limited (ASX: NCC), NAOS Small Cap Opportunities Company Limited (ASX: NSC), and NAOS Ex-50 Opportunities Company Limited (ASX: NAC), and the NAOS Private Opportunities Fund. Robert is also a non-executive director of Ordermentum Pty Ltd.

Robert holds a Bachelor of Business from the University of Technology, Sydney, and a Master of Applied Finance (MAppFin) from the Financial Services Institute of Australasia/Kaplan.

Jared joined NAOS in April 2021 as Senior Investment Analyst. Jared has over 17 years’ financial services experience. Most recently, Jared was an investment analyst at Contact Asset Management and prior to that he spent nine years at Colonial First State.

Jared holds a Bachelor of Commerce majoring in accounting and finance from the University of Notre Dame, Sydney, and is a CFA Charterholder.

Tom joined NAOS in May 2025 and is currently studying a Bachelor of Commerce (Finance) at The University of Sydney, where he has developed a strong interest in investing and portfolio management.

Mohit Kabra is the Chief Financial Officer (CFO) at NAOS Asset Management. Since joining NAOS in 2025, he has been responsible for NAOS's financial strategy and overseeing its operations. With a strong focus on governance, financial planning, and regulatory compliance, Mohit plays a key role in driving NAOS’ strategic direction and long-term success.

With over 17 years at Deloitte Touche Tohmatsu across three continents, Mohit has developed deep expertise in investment management. His experience spans audit, accounting, advisory services, mergers and acquisitions, financial due diligence, business valuations, and capital market transactions.

Mohit is a Certified Public Accountant (CPA) with the Colorado Board of Accountancy and a member of the American Institute of Certified Public Accountants (AICPA). He is also an associate member of the Institute of Chartered Accountants of India and holds a Bachelor of Commerce (Hons.) from the University of Delhi, India.

Rajiv is the Chief Business Officer at NAOS and holds a Bachelor of Laws (First Class Honours), a Bachelor of Business (accounting major) and a Graduate Diploma in Legal Practice from the University of Technology, Sydney.

Rajiv has over 15 years’ experience, having most recently held senior legal roles at Custom Fleet, part of Element Fleet Management (TSX: EFN), and also at Magellan Financial Group (ASX: MFG). He has also previously worked at law firms Johnson Winter & Slattery, and Clayton Utz.

Rajiv is a member of the Law Society of New South Wales and is admitted to the Supreme Court of New South Wales and the High Court of Australia.

Angela joined NAOS in May 2020 in the capacity of Marketing and Communications Manager.

Prior to joining NAOS, Angela held marketing roles for companies in both Australia and the UK, including SAI Global, American Express, Citibank, and Arete Marketing.

Angela holds a Bachelor of Communications majoring in advertising and marketing from the University of Canberra.

To be caretakers of the next generation, we must actively support positive change. Supporting our commitment to ESG issues, NAOS Asset Management (the management company) donates 1% of recurring revenue to the community and the environment.

NAOS is proud to be supporting:

The Board of NAOS Ex-50 Opportunities Company Limited is committed to achieving and demonstrating the highest standards of corporate governance. As such, the Company has adopted what it believes to be appropriate corporate governance policies and practices, having regard to its size and the nature of its activities.

The Board has adopted the ASX Corporate Governance Principles and Recommendations, which are complemented by the Company’s core principles of honesty and integrity. The corporate governance policies and practices adopted by the Board are outlined in the Corporate Governance section of the Company’s website naos.com.au/corporate-governance.

Join our investment community. Be the first to receive NAOS News, Insights and Invitations.