Empower your investment journey with knowledge. Subscribe to NAOS News & Insights.

By subscribing you consent to NAOS using your personal information in accordance with its Privacy Policy, a copy of which is available here.

By subscribing you consent to NAOS using your personal information in accordance with its Privacy Policy, a copy of which is available here.

Understand how LIC profit reserves work, why they're separated from losses, and what to look for when assessing dividend sustainability.

The profit reserve is a feature that appears regularly in the annual reports and dividend announcements of Listed Investment Companies (LICs), but it is not always well understood by investors. It is the account that records a company’s prior-period profits that have been set aside and remain available to be paid out as dividends in future periods. This article explains what a profit reserve is, why it exists, how it works, and what investors can look for when reviewing the profit reserve of a LIC.

A profit reserve is an account within a LIC that records profits earned in prior periods but not yet paid out as dividends. In simple terms, it is a pool of past profits that the company has set aside and is available to fund future dividend payments.

Because a LIC is structured as a company (and not a trust), it can retain profits on its balance sheet rather than being required to distribute all income each year. These retained profits sit in the profit reserve until the Board determines that they should be paid out to shareholders as a dividend.

The two terms are sometimes used interchangeably, and the practical effect for an investor is the same: both describe profits retained from earlier periods that are available to fund future dividends. The label can differ between companies. Some describe the account as a profit reserve and others as a dividend reserve or a dividend profit reserve, but the substance is the same pool of retained, distributable profits. The important point is not the name but what the account represents and how it is disclosed in the financial statements.

Profit reserves exist because of the corporate structure used by LICs. Unlike a managed fund or an exchange traded fund, which are typically structured as trusts and are generally required to distribute all income to investors each year, a LIC is a company and is taxed at the company tax rate on its profits. Once tax has been paid, the after-tax profit is available either to be retained on the balance sheet (in the profit reserve) or paid out as a dividend.

There is also a specific technical reason a LIC segregates profits into a profit reserve. Following amendments to the Corporations Act in 2010 and the Australian Taxation Office’s subsequent guidance in Taxation Ruling TR 2012/5 , current-year profits that are left in retained earnings can be offset against prior-year accumulated losses. Profits that are offset in this way may no longer be available for distribution, and a dividend paid from them may not be frankable. By transferring profits into a separately identified profit reserve, and describing the reserve as such in the financial statements, a LIC preserves those profits as available for distribution and supports their frankability in later periods. The transfer is approved by the Board, typically by resolution at the time the relevant accounts are considered.

A common question is what happens to a LIC’s profit reserve in a year where the portfolio incurs losses. The answer lies in how LICs account for profits and losses separately.

Under the corporate structure used by LICs, profits that have been transferred to the profit reserve are held separately from any accumulated losses, which remain in retained earnings. The profit reserve continues to hold the profits set aside in earlier periods, which remain available for distribution, while accumulated losses are tracked separately in retained earnings rather than reducing the profit reserve.

The practical implication is that a LIC may report a loss in a particular year and still be able to pay a franked dividend from profits that were previously transferred to the profit reserve, provided the relevant solvency and franking account requirements are satisfied. This protection is not automatic. It applies to profits that the Board has deliberately quarantined into the reserve in earlier periods. Current-year profits that are instead offset against accumulated losses are generally treated as no longer available for distribution, unless the directors pass a binding resolution to the contrary at the time the accounts are approved. This is a structural difference between a LIC and a trust-based vehicle, where current-year performance more directly drives the distribution available to investors.

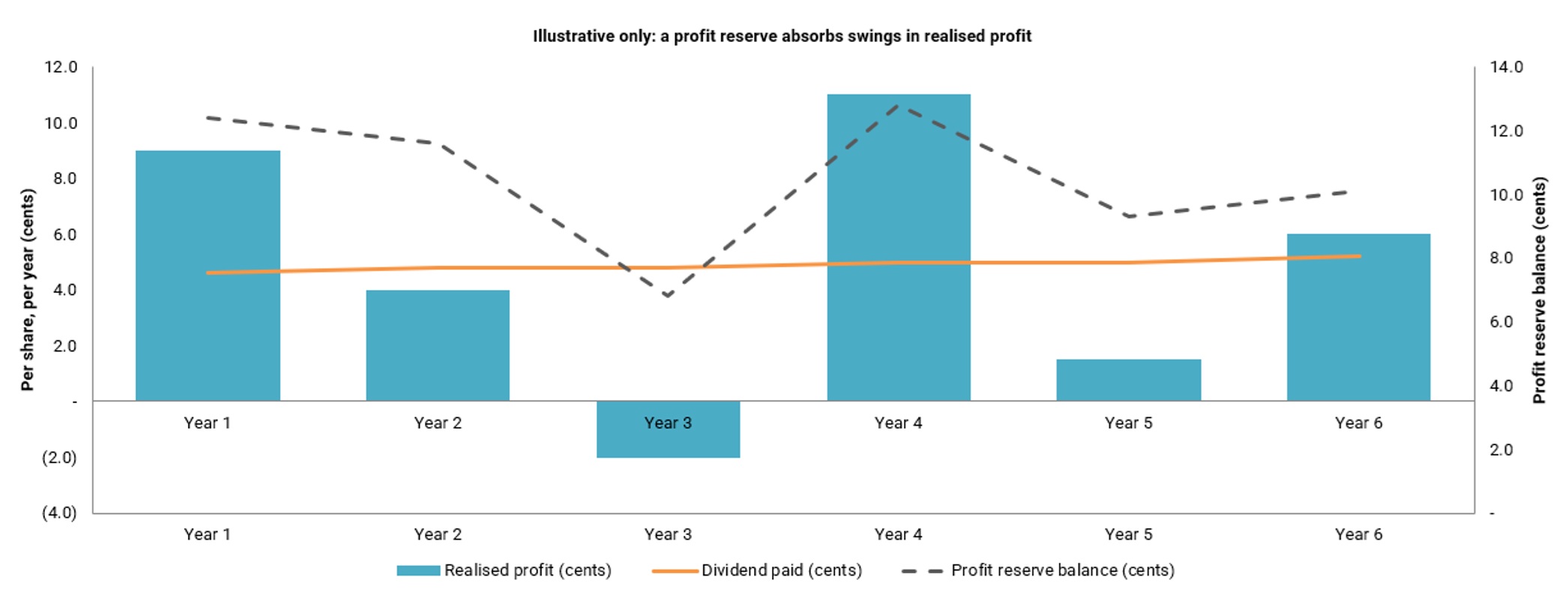

This does not mean losses are without consequence. Sustained or material losses will affect the LIC’s Net Tangible Assets (NTA), its share price, and its ability to generate future profits to replenish the profit reserve. The point is narrower: because profits and losses are held separately, a single weak year does not automatically remove the profit reserve built up in earlier periods, which gives the Board discretion over the timing of dividends through the cycle.

A profit reserve matters to shareholders for three main reasons.

Realised investment returns can vary from year to year. Because a profit reserve holds profits retained from earlier periods, it can give a Board the discretion to determine the timing of dividends across reporting periods rather than tying each dividend directly to the realised result of a single year. Whether a dividend is declared, and at what level, remains a decision for the Board having regard to the available profit reserve, the franking account, solvency, and the company’s dividend policy. A profit reserve does not guarantee a particular dividend or that a dividend will be maintained.

Where a LIC holds a profit reserve, the reserve can form part of the capacity a Board has available to support a dividend in a year in which the underlying portfolio has performed poorly. This is a function of the reserve balance and the matters above, not an assurance that any dividend will be paid or held at a particular level.

In Australia, fully franked dividends carry franking credits, which can provide tax benefits to eligible shareholders. To pay a fully franked dividend, a LIC needs both profits available in its profit reserve and a sufficient balance in its franking account. The two are separate things: the profit reserve represents the profits available to be distributed, while the franking account is a notional tax account that records the company tax already paid and therefore the franking credits available to attach to dividends. The franking account is not a reserve. Reviewing the profit reserve together with the franking account balance gives investors a clearer picture of a LIC’s capacity to continue paying franked dividends.

In our view, the following items can be useful when reviewing the profit reserve of a LIC.

Read it against the LIC’s mandate, portfolio and dividend approach rather than as a single number. It is replenished by new profits each year, and on its own says little about dividend sustainability. The balance appears in the statement of changes in equity and the equity note.

The profit reserve says whether a dividend can be paid; the franking account says whether it can be fully franked. A LIC can hold ample profits but still only partly frank a dividend if franking credits are short. The balance is disclosed in the notes to the financial statements, usually within the dividends or franking note, as the credits available for future periods.

The direction over several reporting periods tells you more than the level at one point. A reserve that is stable or growing suggests profits are keeping pace with dividends; one being steadily drawn down without replenishment cannot continue indefinitely.

Set out in the annual report and on the website, this gives the reserve its context: whether the Board targets a steady or growing dividend, and how it weighs the profit reserve and the franking account. Any dividend remains at the Board’s discretion.

A profit reserve is one of the structural features that distinguishes a LIC from a trust-based investment vehicle. It exists primarily to preserve profits, and their frankability, for distribution in later periods, and it gives a Board discretion over the timing of dividends. It is not a guarantee of future dividends, and the Board retains discretion over whether and when a dividend is declared. For investors assessing a LIC, the profit reserve is most useful when it is read together with the franking account, the underlying portfolio, and the company’s stated dividend policy, rather than on its own.

Join our investment community. Be the first to receive NAOS News, Podcasts, Insights and Invitations.

By subscribing, you consent to NAOS using your personal information in accordance with its Privacy Policy, a copy of which is available here.

Join our investment community. Be the first to receive NAOS News, Insights and Invitations.